Getting the right personal loan can make a noticeable difference when it comes to handling life’s bigger expenses.

For those curious about what Tesco Bank offers, understanding its personal financing options could provide some relief when planning major purchases or consolidating debt.

This article covers what you need to know about Tesco Bank loans . It’s crafted for UK residents evaluating personal loan products, whether for home improvements, new vehicles, or managing multiple repayments.

If your goal is to make informed financial decisions, you’ll likely find practical guidance and realistic insight as you read on.

What Are Tesco Bank Personal Loans?

Tesco Bank provides unsecured personal loans designed to assist individuals with various financial situations.

An unsecured loan means there’s generally no asset, like your home or car, required as collateral. This is typical among high-street banks in the UK, making the process more accessible for many people.

These loans come with defined repayment periods and fixed interest rates. While that sounds straightforward, it’s worth pausing to check what options suit your needs best—loan size, term length, and overall costs all play a role in your decision.

The minimum loan amount typically starts at £1,000, with the maximum often reaching £35,000, but this can change based on your circumstances and eligibility. Repayment terms are flexible, ranging from 1 to 10 years.

The interest rate you receive might be different from the advertised one, as it’s based on a number of factors including your credit history and financial profile.

Key Features of Tesco Bank Personal Loans

Fixed Monthly Repayments

One feature many people appreciate is the fixed monthly repayment structure. This offers some peace of mind as you’ll know exactly how much to budget each month. For those who prefer predictability, this model can take some of the stress out of financial planning.

No Arrangement Fees

Tesco Bank loans usually come without arrangement fees. In practice, that means you won’t see additional upfront charges tacked on to your borrowing. Of course, it’s still necessary to check over the loan agreement to understand if any other costs might apply, like late payment fees.

Early Repayment Flexibility

If you’re considering repaying your loan ahead of schedule, Tesco Bank allows early settlements. However, settling early might result in an interest adjustment or fee, which is quite common in the industry. The advantage is the potential savings on ongoing interest, but as always, checking the terms in the loan agreement is important.

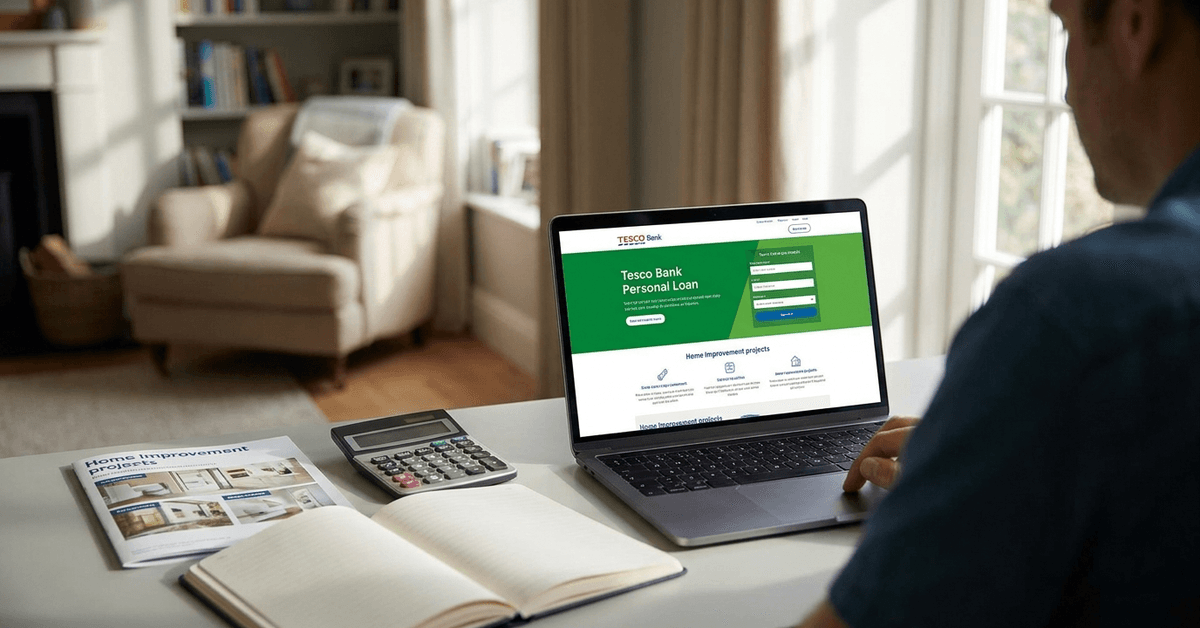

How to Apply for a Tesco Bank Personal Loan

The application process at Tesco Bank is designed to be clear and quick. Applicants can usually check their eligibility online with a soft search—this mostly ensures your credit score won’t be affected at the initial stage.

You’ll need to provide personal and financial details, including your income, employment status, and current credit commitments. Tesco Bank then offers a decision, often within minutes, and if approved, you’ll get a clear picture of the interest rate and terms offered.

If you decide to accept the offer, the final step is to review and sign the agreement. Once complete, funds are transferred—sometimes as fast as within 48 hours. Of course, the actual timeline may vary depending on your circumstances and any additional checks required.

Who Is Eligible for Tesco Bank Loans?

Eligibility for a Tesco Bank loan depends on several criteria. Applicants should typically be UK residents aged 18 or over. You won’t generally qualify if you have an adverse credit history or if your income does not meet their minimum requirements.

The bank also checks employment status and the ability to afford repayments once other financial commitments are factored in. Sometimes, applicants with joint applications might have a better chance, but this depends on both applicants’ circumstances.

It’s also worth noting, Tesco Bank usually lends only to those with a current account and a history of responsible financial behaviour. If you’re unsure if you meet the eligibility criteria, checking directly with the bank or visiting their official loans page might provide additional clarity.

Common Uses for Tesco Bank Personal Loans

Home Improvements

Many borrowers use Tesco Bank loans for home renovations or repairs. These could range from kitchen remodels to structural repairs—whatever fits a household’s priorities. With flexible terms, spreading the cost out is possible.

Debt Consolidation

Sometimes, managing several debts becomes overwhelming. By consolidating existing debts under a single Tesco Bank loan, customers might benefit from lower interest rates or simpler repayment schedules. However, there’s always the consideration that you could pay more interest overall depending on the term and rate chosen.

Major Purchases

Some loans fund large purchases like vehicles, holiday costs, or once-in-a-lifetime family events. While these can be meaningful, it’s wise to evaluate how such borrowing aligns with long-term financial goals. Even small differences in interest rates or terms can make a meaningful impact over the loan period.

Interest Rates and Total Repayment Costs

Interest rates from Tesco Bank are typically advertised as representative APRs. This is the rate that at least 51% of customers receive, but your actual rate could differ based on your financial history.

Calculating the overall cost of a Tesco Bank loan involves more than just looking at the interest rate. Considering the duration of your borrowing and the total repayment amount is just as important. The best way to see accurate figures is with an online loan calculator. Tesco Bank offers a straightforward calculator on their website.

While fixed rates offer predictability, it’s always possible your personal situation changes over a multi-year loan. That’s why some might feel cautious locking in for a longer term, even though payments may be lower month to month. The trade-off is the total interest you’ll pay overall.

Considerations Before Applying

Impact on Credit Score

Taking out any loan, including a Tesco Bank loan, can affect your credit score. Applying for multiple credit products in a short space of time may make lenders hesitant. Ensuring you apply only when necessary might help protect your credit rating.

Ability to Repay

A loan should fit into your budget comfortably. Evaluating all existing financial obligations before committing to any new repayment is usually wise. Some months may be tighter than others; understanding this helps manage expectations.

Lender Reputation and Support

One reassuring point for many is that Tesco Bank is a well-known UK financial institution. Familiar brands can provide some added sense of security, though every lender has its own application process and requirements.

Tesco Bank Loan – Key Facts Table

| Feature | Details |

|---|---|

| Loan Amount | £1,000–£35,000 (subject to status) |

| Repayment Terms | 1–10 years |

| APR Range | Variable; representative APR on website |

| Early Repayment | Allowed, may include fee |

| Arrangement Fees | None |

Where to Learn More and Apply

Those looking to apply or seeking more information can visit the Tesco Bank official loans page. Reading all the small print before making a commitment is sensible. Resources like the Financial Conduct Authority’s loans guidance section can help you evaluate lenders in the UK.

Conclusion – Making Informed Choices with Tesco Bank Loans

Tesco Bank personal loans can be an approachable option for those seeking clear borrowing terms and flexibility. They’re designed to help with a range of purposes, including consolidating debt or funding important purchases.

However, the best personal finance choices usually depend on personal circumstances and priorities, not just product features. Taking some time to consider affordability, eligibility, and alternative solutions is often worthwhile.

Considering information from reputable sources and reflecting on your own needs might help make borrowing less stressful and more successful in the long run.