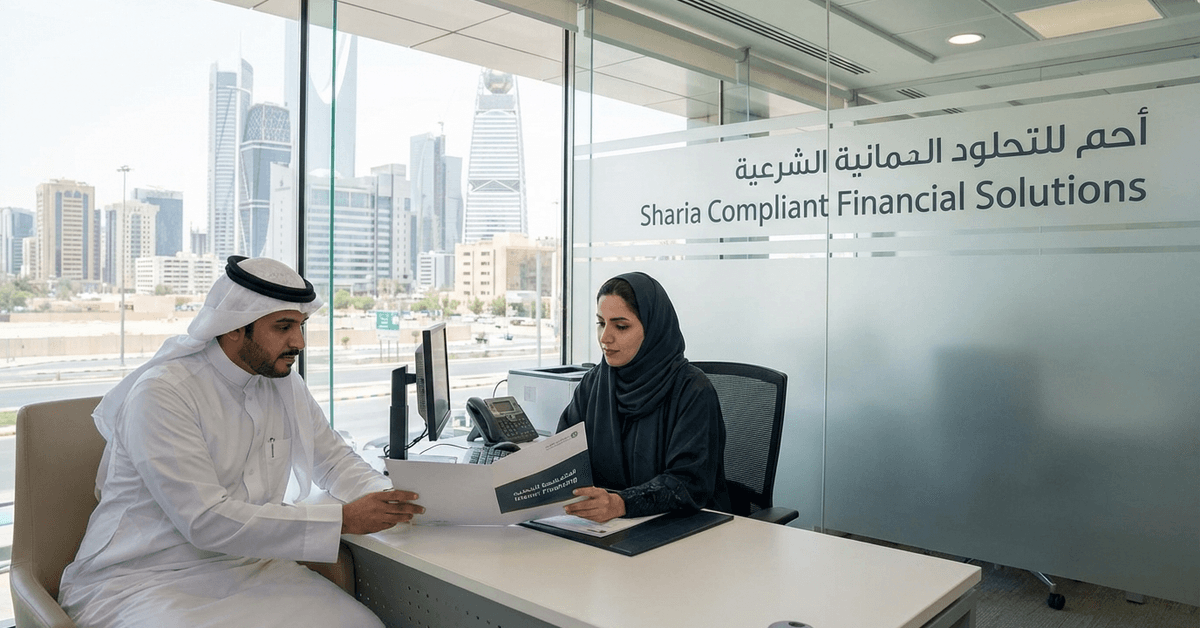

The landscape of Islamic finance in Saudi Arabia is unique and growing. Many people, both locals and expatriates, look for Sharia compliant loans that align with their faith and values.

Exploring how these loans work, who offers them, and what makes them different can help clarify loan options for those seeking alternatives to traditional lending.

This guide is tailored for anyone interested in ethical borrowing practices in Saudi Arabia. Whether you are a resident curious about halal loans or an investor trying to navigate local rules, you’ll find the basics, benefits, and practical tips outlined here.

The aim is to build understanding without promoting any one provider, while keeping cultural sensitivities and financial guidelines in mind.

Understanding Sharia Compliant Finance in Saudi Arabia

Islamic banking follows a strict interpretation of Sharia law. This means all financial products must avoid interest, excessive uncertainty, and investments linked to prohibited industries.

In Saudi Arabia, these rules are enforced not just by banks, but also by regulators and scholars.

Key principles underlie these loans. For instance, charging interest (‘riba’) is not allowed.

Many loans are designed to be transparent, risk-sharing, and asset-backed. It’s what sets them apart from their conventional counterparts. This difference is reflected in both the product design and the customer experience.

Types of Islamic Loans Available in Saudi Arabia

Several products fall under the umbrella of Sharia compliant financing . Each one serves a unique purpose and caters to different needs, whether personal, home, or business-related. Below are some common types you’ll encounter in the Saudi market.

Personal Financing (Tawarruq)

Many banks offer something called ‘Tawarruq.’ In this arrangement, the bank buys a commodity, sells it to the customer at a markup, and the customer immediately sells it for cash. The process follows all Sharia guidelines, ensuring no interest is charged or received.

Home Financing (Murabaha and Ijara)

When it comes to buying a home, Murabaha and Ijara are the typical routes. Murabaha involves the bank purchasing a property and selling it to you with a disclosed profit. Ijara, meanwhile, is more of a lease-to-own arrangement, where you pay rent that includes a gradual purchase of the home.

Business Loans (Musharaka and Mudaraba)

Entrepreneurs and companies often look for Musharaka or Mudaraba arrangements. In Musharaka, both parties contribute capital and share profits and losses. In Mudaraba, one party supplies the capital while the other brings expertise and management.

How Do Sharia Compliant Loans Work?

The workings of Islamic loans can appear complex at first. The key difference lies in the structure and transparency of the agreements. Instead of paying interest, you agree to pay for assets or services at a fixed markup—or share profits in business ventures.

For example, in a Murabaha deal for a car, the bank buys the vehicle first, then sells it to you at a set profit. You pay in installments. This way, the cost of borrowing is clear from the start, and you avoid any hidden charges or riba.

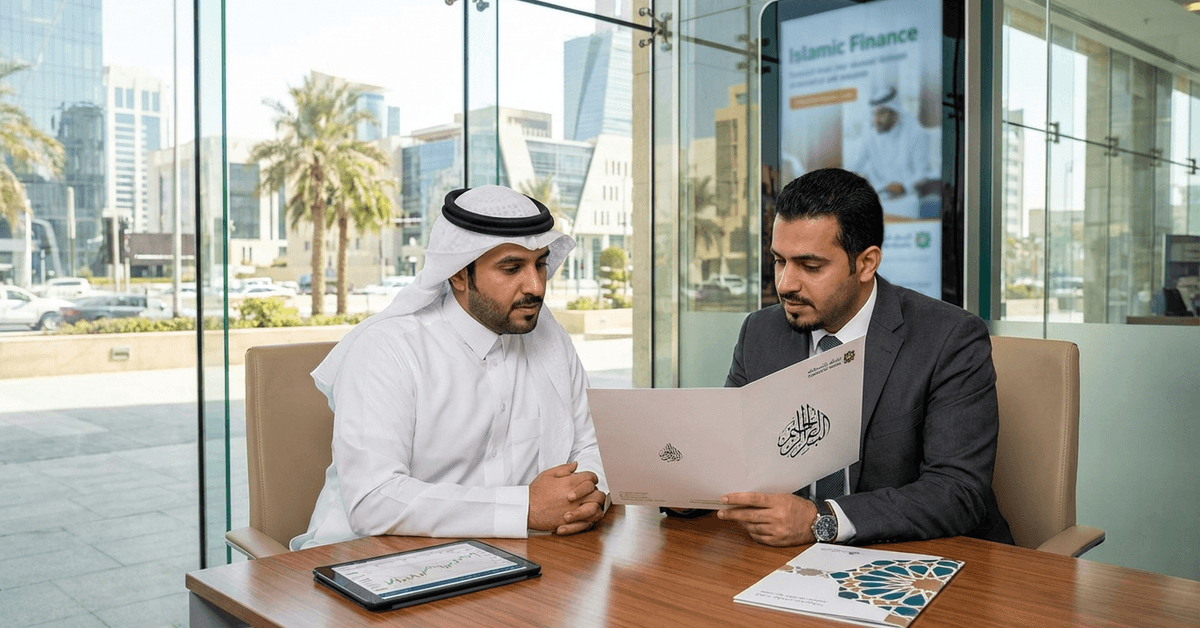

Major Saudi Banks Offering Islamic Loans

Sizable banks across Saudi Arabia offer Sharia-compliant loans. Some operate exclusively on Islamic principles, while others present both conventional and Islamic options. Among the more prominent names are:

- Al Rajhi Bank

- Bank Aljazira

- National Commercial Bank (NCB/AlAhli)

- Samba Financial Group

- Banque Saudi Fransi – Islamic Banking

While all these banks follow Saudi regulations, the actual loan process and benefits may differ from one bank to another. Investigating the details directly with your chosen bank generally leads to the clearest understanding.

Why Opt for Islamic Loans?

There are several reasons people prefer these loans, even beyond religious obligations. Some feel reassured by the ethical, transparent contracts. Others believe the profit-sharing system leads to a fairer economic environment, especially during difficult times.

Islamic loans can also potentially offer protection against certain market risks, since they’re designed for risk-sharing. However, the profit rates and eligibility criteria might sometimes seem stricter compared to conventional loans.

Eligibility and Required Documentation

Applying for a Sharia compliant loan in Saudi Arabia isn’t necessarily complicated, but the documentation process is usually thorough. You will often need:

- Proof of identity (Saudi ID or Iqama)

- Proof of income or employment

- Bank statements (typically last 3–6 months)

- Details of the asset or purpose for financing

While this might sound exhaustive, most banks and lenders in the Kingdom are used to handling these procedures efficiently.

Common Misconceptions Around Sharia Compliant Loans

Some think Sharia financing is limited or complicated. Actually, though, these loans are increasingly mainstream in Saudi Arabia. Most local banks design competitive products that suit both individual and business needs.

Another myth is that Sharia loans are always cheaper than conventional ones. This can be true in some cases, but not always. The total cost will depend on the markup, product type, and your own profile as a borrower.

Legal and Regulatory Considerations

The Saudi Central Bank (SAMA) oversees all financial institutions, including Islamic banks. All products are checked for Sharia compliance by in-house advisory boards and sometimes by national boards.

This strict regulation provides extra assurance to borrowers. But it also means terms and eligibility can change—especially as new financial products come to the market or when global economic conditions shift.

Tips for Choosing the Right Islamic Loan

Choosing a suitable loan comes down to more than just rates. Compare product types, repayment schedules, and bank reputations. Asking about hidden fees, prepayment options, and customer reviews can help.

- Read all contracts in full, even if time-consuming

- Double-check the profit rate and payment structure

- Consult the bank’s Sharia advisor if you have doubts

Many borrowers find it helpful to talk with friends or community members with experience. Sometimes word-of-mouth reveals issues or benefits you won’t see in the brochure.

Potential Challenges with Islamic Loans

It’s fair to admit the process isn’t entirely friction-free. Sometimes the process feels longer than with conventional loans. The markups can occasionally be higher, depending on the product. There may also be less flexibility in some repayment plans.

Still, most people in Saudi Arabia report satisfaction with the ethical and financial clarity provided by these loans. That said, your own experience will depend on your unique needs and the bank’s approach.

Frequently Asked Questions About Saudi Islamic Loans

Are expatriates eligible for Islamic loans in Saudi Arabia?

Most banks do offer Sharia-compliant financing to expatriates, provided they meet basic income and residency requirements.

What happens if I miss a payment on an Islamic loan?

While late payment penalties exist, Sharia law prohibits profiting from these fees. Usually, any penalty is donated to charity, not kept by the bank.

Can I pay off an Islamic loan early?

Pre-payment is generally permitted, but terms can vary. Some banks waive all fees, others may ask for a nominal charge.

Is there such a thing as an “interest-free” loan in Saudi Arabia?

Technically yes, but it’s structured differently—instead of interest, banks earn profits via disclosed markups. The cost becomes a transparent part of the agreement.