Islamic credit cards are becoming increasingly popular in Saudi Arabia, reflecting the unique financial needs and cultural values of the region.

Navigating the options can feel overwhelming at first, but for those concerned with Sharia-compliant banking, these products present alternatives that may align well with everyday financial management.

This article is especially useful for anyone residing in Saudi Arabia, thinking of applying for credit, or exploring personal finance in a halal way.

What Makes a Credit Card Islamic?

The concept of an Islamic credit card centers on Sharia law principles. Conventional credit cards often involve interest payments—commonly termed as riba—which are prohibited in Islamic finance. So, what sets these alternatives apart?

Sharia-Compliant Structure

Islamic cards avoid conventional interest charges by utilizing models such as Murabaha (cost plus profit) or Ujrah (fee-based). The bank buys goods at a customer’s request and sells them at a profit, or charges a transparent fee for services provided.

No Riba (Interest-Free)

Instead of charging monthly or annual interest on outstanding balances, these cards often use pre-agreed fees. It’s simple in concept, yet the practicalities can still vary from one provider to another.

Halal Rewards and Spending

Rewards, if offered, are structured in a manner that does not promote haram (prohibited) spending. And I suppose that adds an extra layer for some users who want both convenience and ethical peace of mind.

Key Features of Islamic Credit Cards in Saudi Arabia

The market for Sharia-compliant cards has grown steadily. Each financial institution seems to tweak its offering a bit, but several features appear frequently:

- No Compounding Interest: Transparent, upfront administration fees replace interest charges.

- Charitable Contributions: Some cards support automatic donations to approved causes with every transaction.

- Halal Merchant Listing: Certain card programs encourage spending at halal-certified merchants or exclude specific industries.

- Global Acceptance: Most major Saudi banks offer cards usable internationally, though sometimes with specific spending restrictions.

- Arabic/English Bilingual Services: Many of the top cards and statements arrive in both languages, easing access for residents and expatriates alike.

How Do Islamic Credit Cards Work?

The process behind an Islamic credit card may seem somewhat technical at first, but the experience for end-users typically feels similar to regular credit cards.

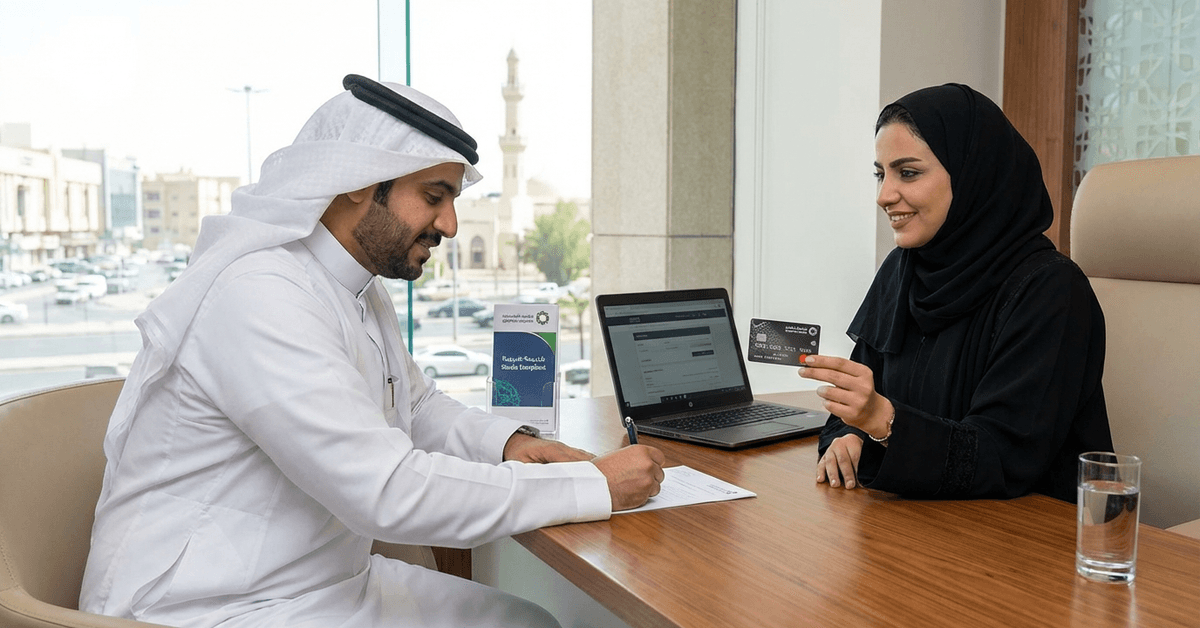

Approval Process

Applicants are usually assessed for their income, credit history, and, in some banks, their compliance with certain Sharia guidelines. Perhaps this sounds familiar—it’s not that different from conventional cards.

Spending and Billing

Once approved, users receive a monthly statement just as with other cards. The difference is the absence of interest on unpaid balances—but there might be a pre-discussed service fee, which is not calculated as a percentage.

Repayment Structures

Some cards operate on a charge-card basis, requiring full repayment, while others allow for monthly installment payments, structured in accordance with Sharia.

Why Islamic Banking Matters in Saudi Arabia

Saudi Arabia’s financial ecosystem is deeply connected to Islamic values. For many, choosing a Sharia-compliant card is not only a matter of faith, but also reflects cultural trust and regulatory standards.

Regulatory Oversight

The Saudi Central Bank (SAMA) sets frameworks to make sure that Islamic finance offerings adhere to both local and international standards. Islamic card providers generally have a Sharia board reviewing their practices.

Cultural Familiarity

Most major Saudi banks are well-versed in Islamic finance. I think for those new to Saudi Arabia or even new to the idea of Islamic banking itself, there’s often an educational curve—but banks usually provide bilingual support and information.

Top Islamic Credit Card Providers in Saudi Arabia

The Saudi market features both local and international banks with strong Sharia-compliant products. While exact rankings vary, consistently notable names include:

- Al Rajhi Bank

- Samba Financial Group

- Banque Saudi Fransi

- Arab National Bank

- SABB (Saudi British Bank)

Each brand offers its own blend of features, service tiers, and sometimes travel or loyalty programs. Not every card suits every customer, though. Some focus on benefits like travel, others on local merchant discounts.

Eligibility and Application Requirements

Application criteria tend to be comparable to standard credit cards, with minor differences depending on the issuing bank:

- Minimum income (ranges from SAR 3,000 to SAR 10,000 per month)

- Valid Saudi or resident ID

- Proof of employment or self-employment

- Clean credit record (sometimes flexibility is shown, but it’s variable)

- Whether the applicant is complying with basic Sharia eligibility (usually, this is reviewed internally by the bank’s Islamic finance board, not something users must prepare for separately)

Potential Advantages of Islamic Credit Cards

Islamic cards promise certain advantages over conventional options, especially for users who wish to remain compliant with their religious beliefs. These may include:

No Interest Charges

Obvious, but perhaps also comforting for those wary about riba in their everyday finances. It’s difficult to overstate how important this can be for some cardholders.

Transparent Fee Structure

Knowing exactly what you’ll pay each month—without percentages or compounding—is, I think, appealing for many.

Ethical Spending Control

The exclusion of non-halal industries or support for charitable causes can serve as a subtle nudge towards mindful spending.

Challenges and Considerations

Of course, even the best-designed products have downsides. A few realities do apply here:

Fee Amounts Versus Interest

While there’s no interest, service fees on Islamic cards may sometimes exceed the equivalent interest you’d pay on a conventional product—especially if spending gets unpredictable.

Rewards Can Be Limited

Because bonuses must comply with Islamic finance rules, cashback and air miles offerings may be narrower or restricted in how they are used.

Merchant Acceptance

Generally, acceptance isn’t an issue within Saudi Arabia. Overseas transactions, however, can occasionally be flagged, depending on the card’s issuer and the region of use.

Frequently Asked Questions

Questions about Islamic credit cards pop up often, such as:

- Is there truly no interest at all? (Generally, yes, provided repayments are made in line with the issuer’s terms.)

- Are annual fees higher? (Sometimes, though, the transparency offsets the lack of interest.)

- What happens if I miss a payment? (Penalties are structured as fixed fees or charitable donations, but not as extra interest.)

- Can expatriates apply? (In most cases, yes, if residency and income criteria are met.)

Conclusion

Islamic credit cards in Saudi Arabia offer exceptional Sharia-compliant banking, genuine interest-free financing, authentic religious compliance, comprehensive merchant acceptance, proven ethical investment principles, authentic rewards, and excellent customer support.

Apply for your Saudi Arabia Islamic credit card today with complete confidence, knowing your thorough preparation and clear Sharia-compliance understanding will help you effectively secure compliant card benefits.